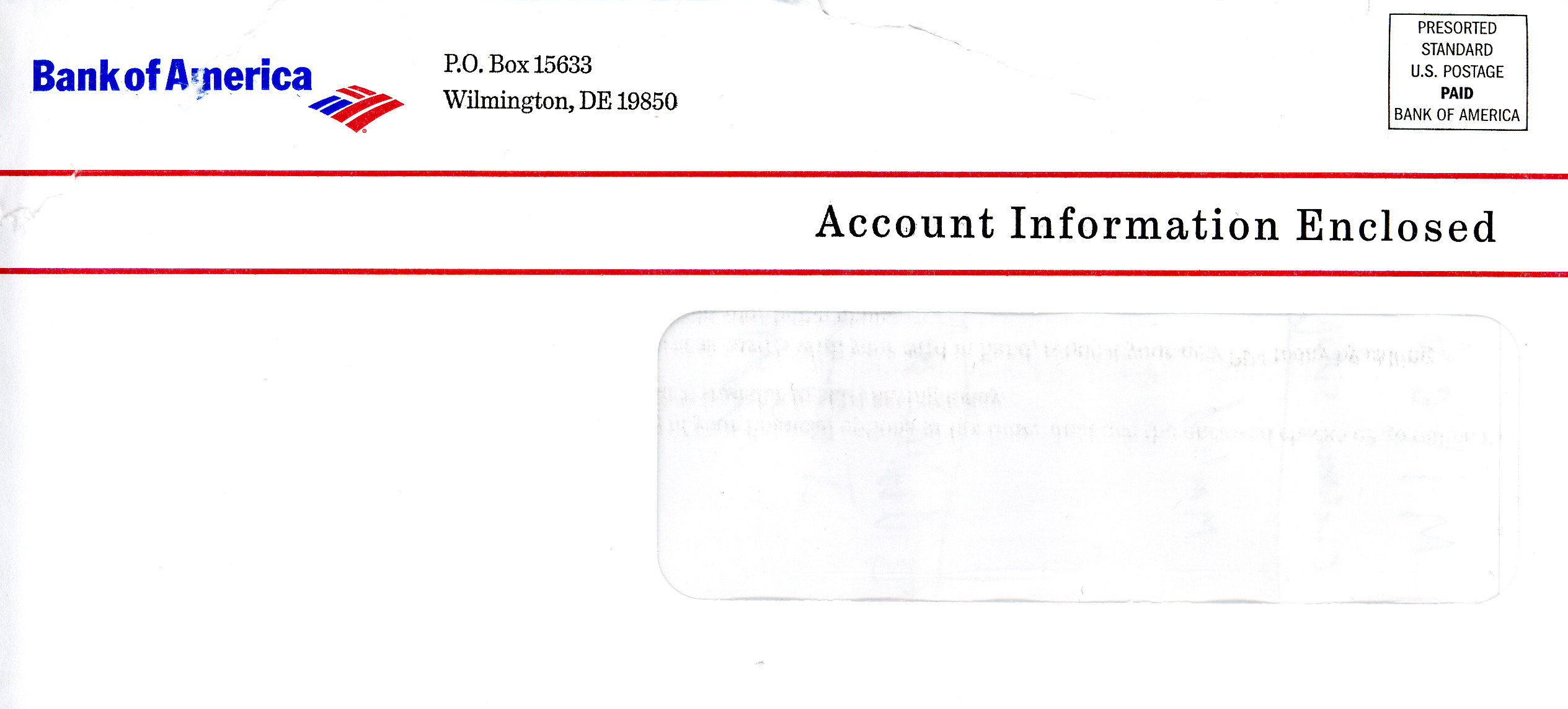

I got a letter from my bank yesterday which came in this envelope:

I opened it, thinking I had a bank statement, or worse (since the next bank statement wasn't due). That's what most people would do, I think, if they got a letter from their bank saying in big letters, “Account Information Enclosed.”

But there wasn't any account information in there, not as I understand the term. Instead there was a page of advertising extorting me to use one of the three enclosed check-like documents to get a cash advance on my credit card which is about the most expensive way to borrow money short of a payday loan.

So I've written a letter to the bank to let off steam. Now the questions are, (1) should I send it, and (2) can it be improved? Full text below.

February 24, 2007

Kenneth D. Lewis

Chairman, Chief Executive Officer and President, Bank of America

Bank Of America Corporate Center

100 N Tryon St

Charlotte Nc 28255

Dear Mr. Lewis:

I am writing you in the hopes that you will put a stop to a deceptive advertising practice that the Bank of America has adopted.

I recently received a letter from Bank of America with a small representation of the American Flag, and the words “Account Information Enclosed” in big letters on the envelope. Of course I opened it at once — who wouldn't? — but was shocked to find that it did not contain any information about my account. Instead it contained an advertisement encouraging me to borrow money via “checks” that serve as a cash advance drawn on my Quantum MasterCard. This is not “account information” as I understand the term. I've asked many other people, and they all agree that “account information” would mean a bank statement or a notice of some kind such as a charge or deposit record or a change in the terms of the account.

I called customer service at 1 800 692 1564 and attempted to speak to someone about this but was not successful. Customer Service offered to stop sending me the blank checks, which is fine but as I tried to explain to them doesn't really get to my main point: I want to do business with a bank that I can trust, and part of that trust is telling me (and other customers) the truth. I don't think this envelope was truthful. The front-line Customer Service agent then tried to tell me that the checks were “account information” because they were linked to my account. That's so silly that I consider it offensive.

When, after about eight requests, I was finally permitted to speak to a supervisor, the very polite gentleman agreed with me that the marketing was deceptive (he said it made him think of Machiavelli!) and said that if it was up to him, he would change it, but that he didn't have the power to do so. I then asked for the name of a person to whom I could address my concerns, but, like the front-line Customer Service before him, the second-line agent was unable to provide me with the name of any human being at the bank who is responsible for these matters. I was offered a chance to write to a generic address, but declined. I prefer to deal with people who have names and believe that people in organizations should take personal responsibility for their decisions.

And that is why I am writing directly to you.

I'm sure you agree with me that the Bank of America wants to avoid trying to trick people in any way, whether small or large. In this, I am heartened by the strong statement online that appears over your signature at [Long URL]:

At Bank of America, we are committed to upholding the highest standards of corporate governance and ethical conduct in all we do.

In its role as our primary governing body, our board of directors provides oversight of the company's affairs and constantly strives to improve and build on the company's strong corporate governance practices.

Our management processes, structures and policies help ensure compliance with laws and regulations and provide clear lines of sight for decision-making and accountability.

… One way we build and protect our culture is by aggressively promoting our company's core values to associates at all times, as well as our Code of Ethics. We also know that actions speak louder than words. And so, we foster a culture of openness, in which healthy debate is encouraged and associates are expected to blow the whistle on improper activity.

Indeed, I congratulate you on fostering a culture in which even a fairly low-level employee feels empowered to identify this deceptive advertising strategy for what it is, Machiavellian.

I also draw great comfort from Bank of America's Code of Ethics at [another long URL], where you state,

Trust is the foundation on which we build strong relationships with our customers, our shareholders, our communities and one another, and it is trust that enables us to achieve our goals. The responsibility for creating and sustaining trust in Bank of America rests squarely on each of us and the personal integrity we bring to our work.

I am sure you will agree that routinely sending out tens of thousands of letters claiming “Account Information Enclosed” when in fact they have no such thing undermines my (and no doubt many other customers') trust in the Bank of America.

I look forward to your prompt attention to this matter, and trust that you will approach it the spirit of the Bank of America motto, “Higher Standards.”

Yours Sincerely,

{kind=link}

I like the parts about employee empowerment, but my larger thought is more that someday this Monolithic Bank will certainly do something *even more* disconcerting, so you might want to save up your rightful indignation for that inevitable occasion.

Don’t send it — why should you help a profit-motivated corporation that seems hell-bent on exploiting its client base?

Pick the credit union of your choice. Fire BAC. Tell all your friends to do the same, and tell them why in great detail.

You’ll probably make money on the deal, even.

You’re making a big deal out of not much. I’d actually rather they keep writing “account information enclosed” on the envelope if they’re going to send me checks that might be subject to theft. That way I’ll be sure to open it and shred those checks immediately.

I’d much rather they not be able to send me those checks, or at least absolve me of liability if someone steals them and uses them to ring up big charges on my account.

You’re making a big deal out of not much. I’d actually rather they keep writing “account information enclosed” on the envelope if they’re going to send me checks that might be subject to theft. That way I’ll be sure to open it and shred those checks immediately.

I’d much rather they not be able to send me those checks, or at least absolve me of liability if someone steals them and uses them to ring up big charges on my account.

Michael, Your letter might be an effective response if this was a one-time aberration but, in my experience, this is really just one more example of legal but unethical behavior by B of A. I’d recommend sending them a letter explaining why you will no longer be doing business with them (“I want to do business with a bank that I can trust”). I admit I was slow when faced with the same choice myself. It wasn’t until they refused to correct an error they had made in the amount of a payment, even after I supplied them with the cancelled check and transaction statement from the other bank involved, that I finally saw the light.

Ryan, You actually don’t have any liability if someone takes those checks and uses them.

Don’t send the letter. Find a class action attorney to have Bank of America see of the error of its ways. Your time and attention are valuable — and B of A is stealing them.

Wouldn’t I have liability if through my negligence I allowed someone else to obtain those checks and forge my signature? That would transform the real defense of forgery/unauthorized signature into a personal defense, which is not good against a Holder in Due Course.

Would it be negligent for me to simply toss the unopened envelope in the garbage rather than open it and shred the checks?

Try https://www5.bankofamerica.com/privacy/Preferences.do

Answer Yes to “Do you want Bank of America to stop sending you marketing information by mail?”

I’m not sure how effective it is, because the fine print says:

If you choose to stop receiving marketing offers by mail, you will continue to:

– Be contacted as necessary to service your account and for other non-marketing purposes

– Be contacted by your client relationship manager or assigned account representative, if applicable

– Receive marketing information included with your regular account mailings and statements, including online and ATM communications

It’s a good letter, and you already wrote it; it’d be a shame to waste it by not sending it (though arguably it’s not a total waste since you blogged about it). Who knows – it might do them some good to get called out for an ethics violation by a law professor.

Send it to the AG, not to BOA!

State AG or federal AG? I’d have thought the appropriate regulator was the Comptroller of the Currency, or maybe the FTC, given that BoA is a national bank (although the credit card is run through a subsidiary).

I think it’s a good letter on the topic…but will it actually have any effect? I wouldn’t hold my breath on that. But just as an aside – From the juxtaposition of the *below the fold* format you used for posting this letter…it appears that you are signing it as Yours Sincerely, « Less Is More

Kinda like a Ben Franklin-ish signature from Citizen *Less is More* on a topic where perhaps *less is more*. 🙂

Take the Postage Paid envelopes that they sometimes include and tape them to a brick and drop them into a mailbox.

No return address needed. Oh, and your finger prints might be on the duct tape, so before you open your mail, put on those cheap painter gloves.

Alas, the brick trick stopped working back in the Nixon administration. Too many people were sending bricks to the CREEP [Committee to Re-Elect the President] so they had the postal service change the rule.

I like the letter. The mailings are odd but pretty easy to tell from account statements because they’re thinner, usually, so we just shred them without opening them now. But the first few times we got them, it was a bit unnerving. If nothing else, your letter might remind the bank of its Kafkaesque customer service / communication process, although it’s not clear that any other bank is any different in this day and age, so there’s no issue of competitive disadvantage here. Except that credit unions don’t tend to do this kind of stuff (I like credit unions).

Michael,

You should be able to find Bank of America’s regulator and additional information here:

http://www2.fdic.gov/idasp/main_bankfind.asp

The regulator is the OCC, but I would seriously advocate locating a local class action shop who will act on that letter. Corporations listen much more closely when they’re forced to spend time and money towards defending themselves. You cannot guarantee that public regulators will act on your letter; your AG (state or federal) is almost certainly not going too, although the primary banking regulator isn’t a bad place to start with.

Why so much fuss? Just serve notice that you will be throwing out unopened all correspondence from them labeled “Account Information Enclosed” as you have no wish for further advertising. Send it certified and get one of those green card receipts.

Actually, I called that same number to get them to stop sending those. As I would in any other call to B of A, I gave them account info to look it up – and then got a weird message about the number being disconnected.

I called the number on the back of the card, and the first number is NOT B of A! Luckily, they flagged my account and won’t accept any more charges. They are sending a new card with a new number as well.

B of A may be crappy, but this one isn’t them.